$232.34

Last最新價 ✓ IBKR · 07-10

Onsite power that runs on a chemical reaction, not a flame — and it's become the fast way to power an AI data center while the grid waits. The reasoning is the model's; every number carries its source and date. 靠化學反應、而非火焰來發電的「現場電廠」 — 在電網大排長龍時,它成了 AI 資料中心最快的供電方式。推論由模型產生,但每個數字都標註來源與日期。

How we analyze this company. A variant-perception deep dive — first understand the business and the technology (jargon decoded below), then ask what consensus may be misreading. Same nine steps as any stock: business → bull → bear → variant view → catalysts → management → moat → probability-weighted odds → what a double takes. The trust rule: no number from memory — each is grounded to a filing or live data with a date, and the share price is recomputed the moment this page is built.

我們是怎麼分析這家公司的。採「變異觀點(Variant Perception)」深度研究 — 先看懂本業與技術(術語在下方解碼),再問市場共識可能誤判了什麼。對任何股票都走同樣九步:本業 → 多方 → 空方 → 變異觀點 → 催化劑 → 經營層 → 護城河 → 機率加權情境 → 翻倍需要什麼。可信規則:沒有任何數字憑記憶寫成 — 每個都標註財報或即時資料與日期,股價在生成這頁的當下即時重算。

The bull case is strong and probably right: AI data centers need power now, the grid takes years, and Bloom's fuel cells deploy in months. But BE is $232.34, +167% YTD, a ~10× run off the 52-week low (✓ IBKR · 07-10), trading at ~113× forward earnings (live price ÷ 2026 guidance EPS ~$2.05). At that multiple the market has still priced years of near-flawless execution.

多方論點很強、而且大概是對的:AI 資料中心現在就要電,電網要等好幾年,而 Bloom 的燃料電池幾個月就能裝好。但 BE 現價 $232.34、年初至今 +167%、從 52 週低點漲約 10 倍(✓ IBKR · 07-10),本益比約 113 倍(即時股價 ÷ 2026 財測 EPS 約 $2.05)。在這個倍數下,市場仍把「未來好幾年近乎完美執行」反映進去。

The question isn't "is the power shortage real" — it is. It's "what's left at 113× earnings, when any execution slip resets the multiple." The asymmetry is less one-sided than it was at 160× — but a July short report moved the live question from the multiple to the backlog itself (scandium supply; $492.6M of binding RPO against a $20B marketed backlog). See the update log up top.

問題不是「電力短缺是不是真的」 — 是真的。問題是 「113 倍本益比之後還剩多少,而任何執行閃失都會讓倍數打回原形」。相較 160 倍時,不對稱性沒那麼一面倒 — 但 7 月一份放空報告,把當下的問題從「倍數」推向「在手訂單本身」(鈧供給;$492.6M 具約束力 RPO vs 對外行銷的 $20B)。詳見上方更新紀錄。

Dated additions, newest first. The core thesis above stays as-is unless an entry says otherwise.

逐則標日期、最新在上。除非條目另外註明,上方核心論點維持不變。

Hedge-fund-backed short seller Hunterbrook Capital published "Bloom's Big Lie" (~07-08) and disclosed a live short. Three load-bearing claims: (1) scandium supply — scaling from ~1 GW to a 5 GW/yr goal would need ~220 tons of scandium oxide against ~240 tons of total global production (China-concentrated), which they call "physically and commercially unattainable"; (2) backlog quality — the ~$20B backlog Bloom markets is >40× the $492.6M binding remaining performance obligations (RPO) in its latest 10-Q, versus a ~2× max gap across the 10 peers they checked; (3) revenue concentration — 74% of Q4'25 revenue from the Brookfield JV. Bloom fired back the next day, calling the report "false and misleading" and saying audited financials, supply chain and scandium access fully support current operations and growth; the stock bounced ~6% on the rebuttal, then fell again. ✓ Hunterbrook / TipRanks / Investing.com · 07-08→09

有避險基金背景的放空機構 Hunterbrook Capital 發布《Bloom's Big Lie》(約 07-08)並揭露持有空單。三個關鍵指控:(1) 鈧(scandium)供給 — 從約 1 GW 擴到 5 GW/年的目標,需要約 220 噸氧化鈧,但全球總產量僅約 240 噸(且集中在中國),他們稱這「在物理與商業上都做不到」;(2) 在手訂單品質 — Bloom 對外行銷的約 $20B 在手訂單,是最新 10-Q 中 $492.6M 具約束力履約義務(RPO)的 40 倍以上,而他們檢視的 10 家同業,最大落差也只有約 2 倍;(3) 營收集中度 — Q4'25 有 74% 營收來自 Brookfield 合資。Bloom 隔天反擊,稱報告「不實且誤導」,並表示已查核財報、供應鏈與鈧的取得完全支撐目前營運與成長;股價因反擊一度反彈約 6%,隨後再跌。✓ Hunterbrook/TipRanks/Investing.com · 07-08→09

Numbers refreshed: price $326.90 → $232.34 (−9.6% on the day, ≈−29% since the 07-01 update) ✓ IBKR · 07-10, +276% → +167% YTD, forward P/E ~160× → ~113× ($232.34 ÷ 2026 guide EPS ~$2.05), market cap ~$93B → ~$66B (~284M sh). 52-wk range now $24.04 → $351.25 (the old $21.53 low rolled out of the trailing window); price sits ~34% below the high.

數字已更新:股價 $326.90 → $232.34(當日 −9.6%,較 07-01 更新約 −29%)✓ IBKR · 07-10、年初至今 +276% → +167%、預估本益比 約 160 倍 → 約 113 倍($232.34 ÷ 2026 財測 EPS 約 $2.05)、市值 約 $93B → 約 $66B(約 2.84 億股)。52 週區間現為 $24.04 → $351.25(舊的 $21.53 低點已滾出滾動視窗);距高點約 −34%。

Does it change the finding? Yes — it splits in two. Valuation: the drop cut the forward multiple 160× → ~113×, so the "priced for perfection" gap the headline flags has narrowed ~30% — the pure over-valuation objection is weaker than on 07-01. Thesis: but the report reframes the bear case from "too expensive" to "are the two pillars real" — the scale-up (scandium) and the backlog ($492.6M binding vs $20B marketed). Those aren't multiple questions, they're does-the-growth-exist questions — and the growth is what justifies any premium. So the decision is no longer mainly about price; it's thesis integrity: refute the scandium + RPO-gap claims and this is a ~29%-cheaper entry on an intact story; can't refute them, and the sell-off is the market pricing a real question, not an overreaction — where adding "because it's lower" is averaging down into an unresolved thesis. Narrative ≠ verified delivery. ◆ framing = judgment定位=判斷

有改變結論嗎?有 — 而且一分為二。估值面:這波下跌把預估本益比從 160 倍壓到約 113 倍,headline 點名的「完美定價」落差收斂約 30% — 純「太貴」的反對,比 07-01 時弱。論點面:但這份報告把空方理由從「太貴」改寫成「兩根支柱是不是真的」 — 擴產(鈧)與在手訂單($492.6M 具約束力 vs $20B 對外行銷)。這不是倍數問題,是「成長到底存不存在」的問題 — 而成長正是撐起任何溢價的東西。所以現在的決策重點不再主要是價格,而是論點完整性:能反駁鈧與 RPO 落差這兩點,這就是故事未破、便宜約 29% 的進場;不能反駁,這波下跌就是市場在為一個真實問題定價、而非過度反應 — 此時「因為變便宜就加碼」就是往未解的論點裡攤平。故事 ≠ 已驗證的兌現。◆ framing = judgment定位=判斷

Brookfield and Bloom expanded their framework to build and finance onsite power for AI data centers from $5B to $25B — a 5× increase (the original $5B dates to Oct 2025). The money sits inside Brookfield's dedicated AI Infrastructure Fund (launched Nov 2025, ~$100B deploy target). ✓ Bloom IR / BusinessWire · 06-30 It is a financing framework — capacity to fund projects, not booked orders; no revenue guidance or backlog figure was attached.

Brookfield 與 Bloom 把「為 AI 資料中心建置並融資現場電力」的框架從 $5B 擴大到 $25B — 5 倍(原本的 $5B 是 2025 年 10 月)。這筆錢放在 Brookfield 專屬的 AI 基礎設施基金(2025 年 11 月成立,目標部署約 $100B)。✓ Bloom IR/BusinessWire · 06-30 這是融資框架 — 是「有能力出資」、不是已簽訂單;沒有附上任何營收財測或在手訂單數字。

Numbers refreshed: price $279 → $326.90 (+7.99% on the day) ✓ IBKR · 07-01, +276% YTD, forward P/E ~136× → ~160× ($326.90 ÷ 2026 guide EPS ~$2.05), market cap ~$79B → ~$93B (~284M sh). Now ~15× off the 52-wk low ($21.53) and only ~7% below the $351.25 high.

數字已更新:股價 $279 → $326.90(當日 +7.99%)✓ IBKR · 07-01、年初至今 +276%、預估本益比 約 136 倍 → 約 160 倍($326.90 ÷ 2026 財測 EPS 約 $2.05)、市值 約 $79B → 約 $93B(約 2.84 億股)。目前從 52 週低點($21.53)漲約 15 倍,距 $351.25 高點僅約 7%。

Does it change the finding? Direction, no — the gap widened. The expansion is a real positive: it directly softens the bear case's financing leg (Brookfield supplies the capital customers would otherwise raise) and signals sustained hyperscaler demand. But it is optionality-to-fund, not orders — and the ~8% pop lifted the forward multiple to ~160×, so the price more than absorbed the news in a day. "A real story, priced for years of flawless execution" holds, and on valuation it's now more stretched, not less. Optionality ≠ catalyst booked. ◆ framing = judgment定位=判斷

有改變結論嗎?方向上沒有 — 而且落差擴大。這次擴大是實打實的正面:它直接減輕空方的「融資」那條腿(客戶原本要自己籌的錢,現在 Brookfield 出)並顯示雲端大廠需求持續。但這是「有能力出資」的選擇權、不是訂單 — 而約 8% 的跳漲已把預估本益比推到 約 160 倍,一天內股價就把利多不只反映完。「故事是真的、但已被定價成未來好幾年完美執行」的結論維持,估值面反而更緊、不是更鬆。選擇權 ≠ 已入袋的催化劑。◆ framing = judgment定位=判斷

Re-pulled live: $279.00, +221% YTD ✓ IBKR · 06-30 — essentially flat vs the $274.86 build. But the 52-week range widened to $21.53 → $351.25: the stock spiked ~28% to a $351 high and round-tripped back, leaving it ~21% below the high. Forward P/E is ~136× ($279 ÷ 2026 guide EPS ~$2.05); market cap ≈$79B (~284M sh). Q1'26 was a beat — non-GAAP EPS $0.44 vs ~$0.13 consensus, revenue +130% ✓ Q1'26 release / Yahoo · ~06-26.

即時重抓:$279.00、年初至今 +221% ✓ IBKR · 06-30 — 相對生成時的 $274.86 幾乎持平。但 52 週區間擴大到 $21.53 → $351.25:股價曾飆約 28% 到 $351 高點又跌回來,目前距高點約 21%。預估本益比約 136 倍($279 ÷ 2026 財測 EPS 約 $2.05);市值約 $79B(約 2.84 億股)。Q1'26 優於預期 — 非 GAAP EPS $0.44,市場共識約 $0.13、營收 +130% ✓ Q1'26 財報/Yahoo · 約 06-26。

Does it change the finding? No. A net-flat price at the same ~136× keeps the headline intact: a real story, priced for years of flawless execution, where the edge is in execution surprises, not the idea. If anything the round-trip to $351 and back demonstrates the "any slip resets the multiple" fragility the bear case flags — a ~28% swing with no change in the long-term thesis. The Q1 EPS beat is a genuine positive (operating leverage showing up), but it's consistent with the price, not a reason to re-rate higher from 136×. ◆ framing = judgment定位=判斷

有改變結論嗎?沒有。股價淨持平、仍在約 136 倍,結論不變:故事是真的,但已被定價成「未來好幾年完美執行」,超額來自執行面的驚喜、而非這個想法。甚至這趟「衝到 $351 又跌回」正好示範了空方點名的「一閃失、倍數就打回」的脆弱 — 長期論點沒變,股價卻能來回約 28%。Q1 EPS 優於預期是實打實的正面(營運槓桿開始顯現),但這與現價一致,不是它該從 136 倍再往上重估的理由。◆ framing = judgment定位=判斷

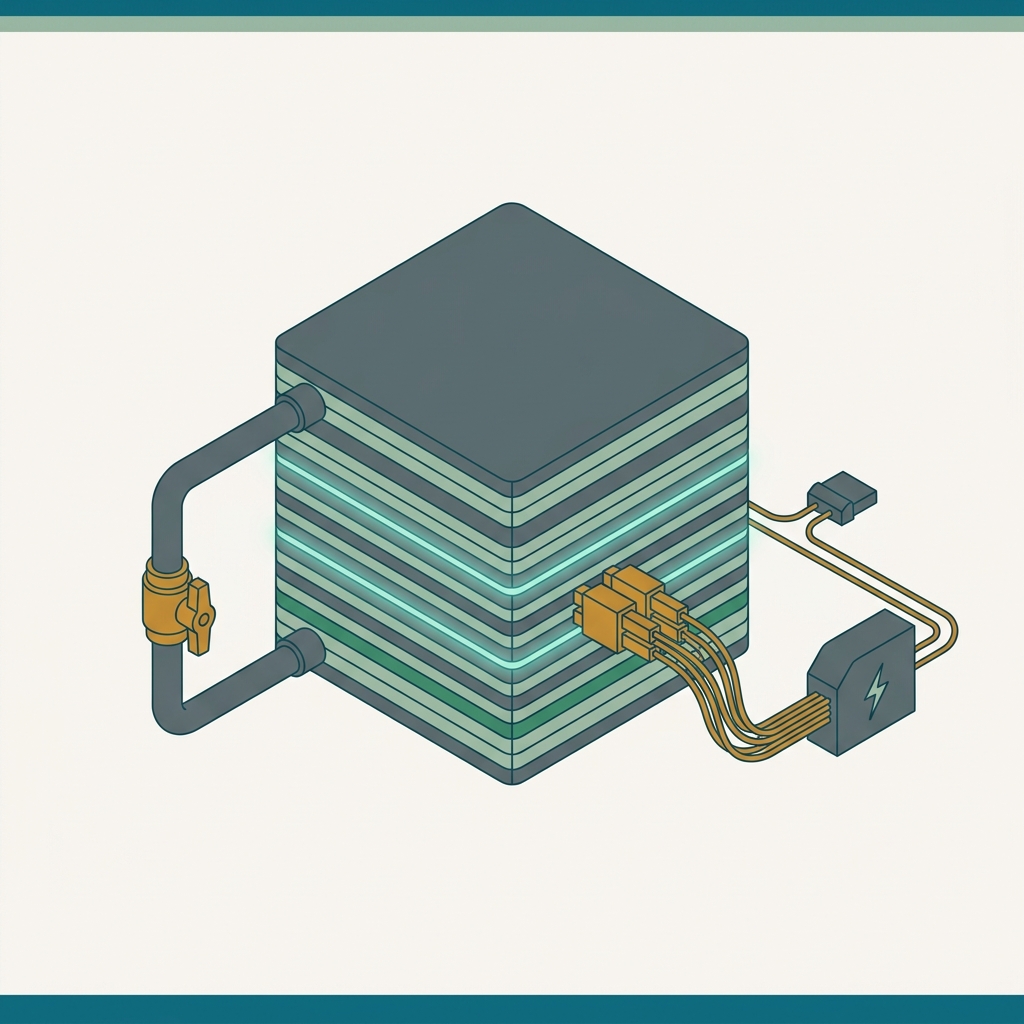

Bloom's box is a solid oxide fuel cell (SOFC). It turns fuel into electricity through a chemical reaction — no burning, no flame — which is why it's efficient, quiet and clean. Here's the reaction, then a plain-language glossary.

Bloom 的箱子是固態氧化物燃料電池(SOFC)。它靠化學反應把燃料變成電 — 不燃燒、沒有火焰 — 所以高效、安靜又乾淨。先看反應,再看白話術語表。

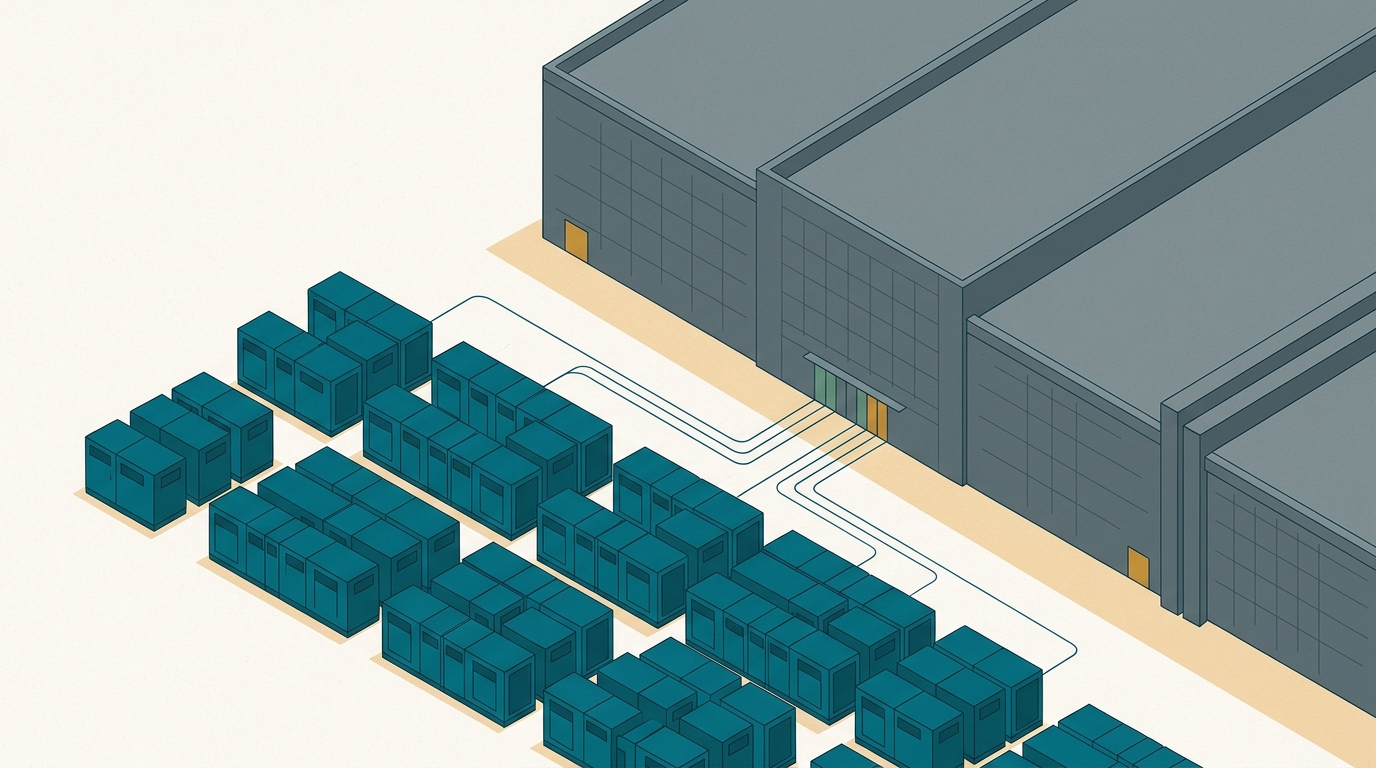

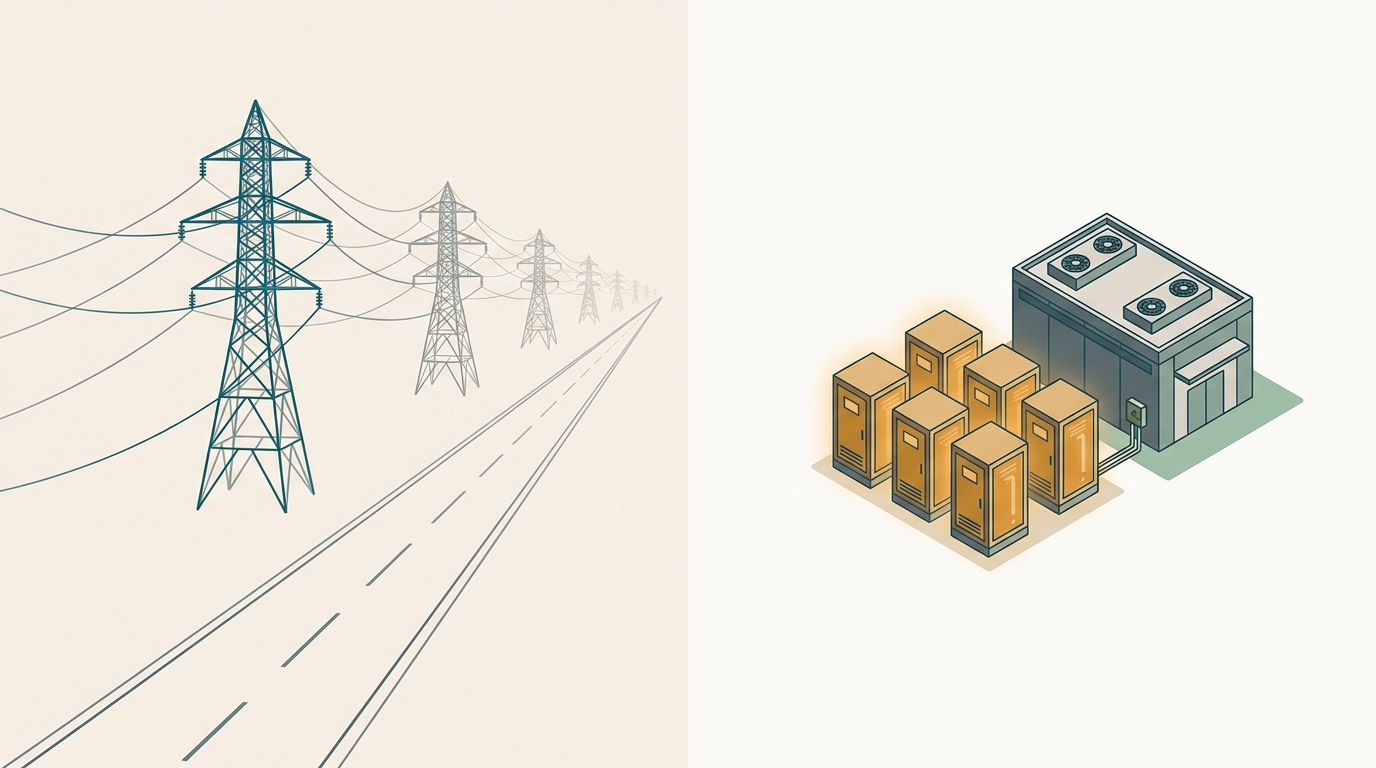

Three pictures for the parts that are easier to see than read:

有三件事,用看的比用讀的更清楚:

AI compute is bottlenecked on power, not chips. New grid hookups take years; Bloom delivers reliable 24/7 baseload onsite in months, cleanly and quietly. That speed-to-power is the whole thesis.

AI 算力的瓶頸是電,不是晶片。接新電網要好幾年;Bloom 幾個月就能在現場供應可靠的 24/7 基載,乾淨又安靜。這個「供電速度」就是整個論點。

Oracle: up to 2.8 GW (1.2 GW contracted) — the validation that re-rated the stock.Oracle:上看 2.8 GW(已簽 1.2 GW)— 讓股價重估的背書。 ✓ PR

Grid bottlenecks last years. Bloom's speed, reliability (up to "five nines"), and fuel flexibility make it the prime onsite answer. Oracle (2.8 GW) is validation; more hyperscaler deals can follow fast.

電網瓶頸會持續好幾年。Bloom 的速度、可靠度(高達「五個 9」)與燃料彈性,使它成為現場供電的首選。Oracle(2.8 GW)是背書;更多雲端大廠訂單可能很快跟進。

Every box shipped adds sticky, higher-margin LTSA revenue. As the installed base compounds, recurring service smooths the cycle and lifts margins.

每多裝一台,就多一份黏著、較高毛利的 LTSA 收入。裝機量複利成長,重複性服務平滑循環、拉高毛利。

Manufacturing scale-up (multi-GW) unlocks operating leverage. 2026 guide already lifts non-GAAP GM toward ~34% and op income to $600–750M.

產能擴張(多 GW)釋放營運槓桿。2026 財測已把非 GAAP 毛利拉向 ~34%、營業利益到 $600–750M。

Electrolyzers + fuel cells position Bloom for green-hydrogen production and use — upside not in the core product numbers. Plus Korea (SK) and broader C&I/microgrid markets.

電解槽+燃料電池讓 Bloom 卡位綠氫的生產與使用 — 這塊上檔不在核心產品數字裡。另有韓國(SK)與更廣的商工/微電網市場。

~113× forward earnings after a ~10× run. Any growth wobble or margin miss compresses the multiple hard. The price still assumes years of near-perfect execution. live · 07-10

漲約 10 倍後仍約 113 倍預估本益比。成長一閃失或毛利不如預期,倍數就大幅收縮。股價仍假設未來好幾年近乎完美執行。即時 · 07-10

Rapid manufacturing ramp + long install cycles. A $20B backlog only matters if it converts — a July 2026 short report notes it is >40× the $492.6M of binding RPO on the balance sheet, plus a scandium-supply constraint on the 5 GW scale-up. A quality issue in a high-stakes AI deployment would also hurt the brand badly.

產能要快速拉升,安裝週期又長。$20B 在手訂單要能兌現才算數 — 2026 年 7 月一份放空報告指出,它是資產負債表上 $492.6M 具約束力 RPO 的 40 倍以上,另有 5 GW 擴產的鈧供給限制。在高風險的 AI 案場出品質問題,也會嚴重傷害品牌。

Gas turbines (established, long lead times), batteries/storage hybrids, grid upgrades, and longer-term nuclear/SMRs all compete for the same "power the data center" budget.

燃氣渦輪(成熟、交期長)、電池/儲能混搭、電網升級,以及較長期的核能/SMR,都在搶同一筆「給資料中心供電」的預算。

Natural-gas price swings, tightening carbon rules, reliance on tax credits, and customers needing to finance large systems. An AI-capex slowdown would hit demand directly.

天然氣價格波動、碳規趨嚴、依賴稅務抵免,以及客戶要為大型系統融資。AI 資本支出一放緩,需求直接受衝擊。

Must hold for the thesis to fail:論點要被推翻,需同時成立: sustained hyperscaler demand, on-time backlog monetization at scale, continued margin expansion, no major competitive or regulatory setback. Break one and a ~113× multiple unwinds fast.雲端大廠需求持續、在手訂單能規模化準時變現、毛利持續擴張、沒有重大競爭或法規挫折。任一條斷掉,約 113 倍的倍數會很快回吐。

No — same "clean/reliable power" universe, different jobs. BE generates power (fuel cells, 24/7 onsite). EOSE stores power (zinc batteries, 3–12h). They're complements (fuel cell + battery in a microgrid), not substitutes. BE is far more advanced commercially (~$2B+ revenue, profitable path, $20B backlog); EOSE is a smaller, higher-risk pure-play storage story.

不一樣 — 同屬「乾淨/可靠電力」範疇,但工作不同。BE 是發電(燃料電池,現場 24/7)。EOSE 是儲電(鋅電池,3–12 小時)。兩者是互補(微電網裡燃料電池+電池),不是替代。BE 商業化遠更成熟(營收 $2B+、有獲利路徑、$20B 在手訂單);EOSE 規模較小、執行風險較高,是純儲能題材。

No. HVDC (high-voltage DC) is long-distance grid transmission — the domain of Hitachi Energy, Siemens Energy, GE Vernova. Bloom is onsite generation, which actually reduces the need for new HVDC lines. Bloom does talk about facility-level DC architectures inside data centers (~400–800V DC busways for GPU racks) — but that's in-building distribution, not grid HVDC. This strengthens the bull case: data centers go onsite to bypass slow grid + transmission build-out.

沒有。HVDC(高壓直流)是長距離電網輸電 — 那是 Hitachi Energy、Siemens Energy、GE Vernova 的領域。Bloom 是現場發電,反而降低了對新 HVDC 線路的需求。Bloom 確實有談資料中心內部的直流架構(給 GPU 機櫃的約 400–800V 直流匯流排)— 但那是建築內配電,不是電網 HVDC。這反而強化多方論點:資料中心走現場供電,繞開緩慢的電網與輸電建設。

Founder-CEO KR Sridhar ✓ public — deep technical roots (NASA / space-tech origins), drove the pivot into the data-center/AI market. Insiders own ~2–3%; net sellers (~$83M net sold last 12 months), no major buying ✓ SWS — a mild negative near the highs.

創辦人執行長 KR Sridhar ✓ 公開 — 技術底子深(NASA/太空科技出身),主導轉向資料中心/AI 市場。內部人持股約 2–3%;淨賣方(過去 12 個月淨賣約 $83M),無重大買進 ✓ SWS — 在高檔屬輕微負面。

Proprietary SOFC IP + system-integration know-how, a proven reliability record, and a growing installed base with sticky LTSA service. Modular design + fuel flexibility are hard to copy fast. The clear leader in behind-the-meter prime fuel-cell power.

專有 SOFC 智財+系統整合 know-how、已驗證的可靠度紀錄,加上不斷成長、帶黏著 LTSA 服務的裝機基礎。模組化+燃料彈性難以快速複製。表後主力燃料電池供電的明確龍頭。

To double from $232.34 (~$132B market cap) needs revenue toward $8–12B+ by the late 2020s with 20%+ operating margins and the market keeping a premium growth multiple. A rising stock has two engines — earnings growth and multiple expansion; at ~113× the second engine is still well past redline, so a double rests almost entirely on delivering the backlog at scale.

從 $232.34 翻倍(約 $132B 市值)需要營收在 2020 年代後期衝向 $8–12B+、營業利益率 20%+,而且市場願意維持高成長倍數。股票上漲靠兩個引擎 — 獲利成長與評價擴張;在約 113 倍下,第二個引擎仍遠超過紅線,所以翻倍幾乎全得靠規模化兌現在手訂單。

| Claim主張 | Verdict判定 | Value · source · date數值 · 來源 · 日期 |

|---|---|---|

| Live price / YTD / range即時股價/YTD/區間 | ✓ | $232.34, +167% YTD, 52-wk $24.04–$351.25 (IBKR 2026-07-10) |

| Market cap市值 | ✓ | ≈$66B (live $232.34 × ~284M sh; shares 284.4M Cl-A, 424B7 2026-04) |

| Forward P/E預估本益比 | ✗→ | ~113× (live $232.34 ÷ 2026 guide EPS ~$2.05) |

| Brookfield financing partnershipBrookfield 融資合作 | ✓ | $5B → $25B (5×), framework to build/finance AI-infra power (Bloom IR / BusinessWire 2026-06-30)$5B → $25B(5 倍),建置/融資 AI 基礎設施電力框架(Bloom IR/BusinessWire 2026-06-30) |

| FY2025 revenue | ✓ | $2.02B, +37.3% (FY25 release 2026-02-05) |

| Q1 2026 revenue | ✓ | $751.1M, +130.4%; product +208%; non-GAAP EPS $0.44 (Q1'26 release) |

| 2026 guidance | ✓ | rev $3.4–3.8B · GM ~34% · op inc $600–750M · EPS $1.85–2.25 (Q1'26) |

| Backlog | ✓ | ~$20B total, ~$6B product (2.5× YoY) (Q1'26) |

| Hunterbrook short reportHunterbrook 放空報告 | ◆ | scandium ~220t needed vs ~240t global; $20B backlog vs $492.6M binding RPO (>40×); 74% Q4'25 rev from Brookfield JV; Bloom rebuts "false & misleading" (Hunterbrook / TipRanks / Investing.com 2026-07-08→09)鈧約需 220 噸 vs 全球約 240 噸;$20B 在手 vs $492.6M 具約束力 RPO(40 倍以上);Q4'25 有 74% 營收來自 Brookfield 合資;Bloom 反駁「不實且誤導」(Hunterbrook/TipRanks/Investing.com 2026-07-08→09) |

| Oracle deal | ✓ | up to 2.8 GW (1.2 GW contracted); Project Jupiter NM up to 2.45 GW (BE/Oracle PR 2026) |

| SOFC mechanism + efficiencySOFC 原理+效率 | ✓ | electrochemical, no combustion; ~50–65% vs turbine ~30–38%電化學、無燃燒;約 50–65% vs 渦輪約 30–38% (Wikipedia/ScienceDirect) |

| Module size / deploy time模組規格/安裝時間 | ⚠ | ~325 kW / ~90 days — company-stated, not independently verified公司宣稱,未獨立查證 |

| Insider ownership / activity內部人持股/動向 | ✓ | ~2–3% owned; net sellers ~$83M last 12mo (Simply Wall St) |

| CEO | ✓ | KR Sridhar, founder (NASA / space-tech) (public) |

| Probability split機率分布 | ◆ | 45/40/15 — draft judgment, not data草稿判斷,非資料 |